Wednesday, September 29, 2010

Classroom Lesson: The Phillips Curve

Here is something I lifted from an old PowerPoint presentation created by Mike Bryan (currently at the Atlanta Fed). Mike is an astute economist with a wonderful sense of humor (how rare is that these days?). These few slides (part of a longer presentation) deal with the Phillips Curve. The file is available here: Orion.

Monday, September 27, 2010

Despite Economy, Americans Don't Want Farm Work

The article is here: Despite Economy, Americans Don't Want Farm Work.

There is, evidently, plenty of agricultural work available in the state of California these days. It's hard work--the type of work most of humanity throughout history had little choice but to perform. And by modern standards, the pay is not that great ($10.25/hr); though our distant ancestors might have considered it astronomically high. Indeed, it is high enough even today to attract a large body of foreign workers (largely from Mexico).

What is it that makes a foreign worker willing to go through all the risk and expense of taking such jobs, when an unemployed domestic worker will not?

A labor economist might answer this question by appealing to differences in reservation wages (an individual's reservation wage is defined to be the lowest wage he or she is willing to work for). Evidently, Mexican migrants have low reservation wages relative to their American counterparts. Another way of saying this is that the former group are relatively "desperate." Yet another way of saying this is that American workers can better afford spells of unemployment--they are generally wealthier, and many can draw on UI to make their job search less painful (and presumably, more productive too).

What interests me about the anecdotal evidence reported in this article is what it implies about theories that explain the current high rate of U.S. unemployment as the consequence of a "lack of aggregate demand" leading to a lack of available jobs. I am not sure how well this hypothesis squares up against the sort of evidence reported in this article. On the surface, at least, it appears that jobs are clearly available; Americans just don't want them--they are searching, or waiting, for better opportunities to arise. To me, the rise in unemployment smacks more of mismatch following a structural realignment of sectoral demands, as opposed to an overall decline in aggregate demand (the latter might explain the decline in employment, but not necessarily the increase in job search activity).

Update 1

When I posted this, I was unaware of Paul Krugman's article this morning: Structure of Excuses. Steve Williamson comments on Krugman here: It's the Housing, Stupid. This is certainly shaping up to be an interesting debate. I would love to see Kocherlakota and Krugman square off against each other in a public debate, but that's not likely to happen any time soon. Too bad.

Update 2

I have work to do, really I do. But I can't quite lay this to rest just yet. Krugman does not put much currency in the "structural" unemployment view. He says:

Hmm....that "Stuck in the Middle" figure sure looks like a negative aggregate demand shock alright. Or how about the next figure? How can it be that firms (not the government, you will notice) are having trouble filling their openings? Where does this show up in Krugman's IS-LM model, I wonder? Just asking.

Hmm....that "Stuck in the Middle" figure sure looks like a negative aggregate demand shock alright. Or how about the next figure? How can it be that firms (not the government, you will notice) are having trouble filling their openings? Where does this show up in Krugman's IS-LM model, I wonder? Just asking.

Here is some more stuff: America's Strongest Job Markets. But of course, it should not be possible to rank domestic job markets in this manner...it's aggregate demand, stupid.

What am I missing here? Is there a legitimate debate to be had, or not? Krugman appears to think not. He is acting more like someone who wants to stifle debate, rather than promote it.

Caveat emptor, I guess.

There is, evidently, plenty of agricultural work available in the state of California these days. It's hard work--the type of work most of humanity throughout history had little choice but to perform. And by modern standards, the pay is not that great ($10.25/hr); though our distant ancestors might have considered it astronomically high. Indeed, it is high enough even today to attract a large body of foreign workers (largely from Mexico).

What is it that makes a foreign worker willing to go through all the risk and expense of taking such jobs, when an unemployed domestic worker will not?

A labor economist might answer this question by appealing to differences in reservation wages (an individual's reservation wage is defined to be the lowest wage he or she is willing to work for). Evidently, Mexican migrants have low reservation wages relative to their American counterparts. Another way of saying this is that the former group are relatively "desperate." Yet another way of saying this is that American workers can better afford spells of unemployment--they are generally wealthier, and many can draw on UI to make their job search less painful (and presumably, more productive too).

What interests me about the anecdotal evidence reported in this article is what it implies about theories that explain the current high rate of U.S. unemployment as the consequence of a "lack of aggregate demand" leading to a lack of available jobs. I am not sure how well this hypothesis squares up against the sort of evidence reported in this article. On the surface, at least, it appears that jobs are clearly available; Americans just don't want them--they are searching, or waiting, for better opportunities to arise. To me, the rise in unemployment smacks more of mismatch following a structural realignment of sectoral demands, as opposed to an overall decline in aggregate demand (the latter might explain the decline in employment, but not necessarily the increase in job search activity).

Update 1

When I posted this, I was unaware of Paul Krugman's article this morning: Structure of Excuses. Steve Williamson comments on Krugman here: It's the Housing, Stupid. This is certainly shaping up to be an interesting debate. I would love to see Kocherlakota and Krugman square off against each other in a public debate, but that's not likely to happen any time soon. Too bad.

Update 2

I have work to do, really I do. But I can't quite lay this to rest just yet. Krugman does not put much currency in the "structural" unemployment view. He says:

After all, what should we be seeing if statements like those of Mr. Kocherlakota or Mr. Clinton were true? The answer is, there should be significant labor shortages somewhere in America — major industries that are trying to expand but are having trouble hiring, major classes of workers who find their skills in great demand, major parts of the country with low unemployment even as the rest of the nation suffers. None of these things exist.Well, I'm not sure if none of these things exist as he claims. Consider, for example, this WSJ article: Some Firms Struggle to Hire Despite High Unemployment. Here is an excerpt:

In Bloomington, Ill., machine shop Mechanical Devices can't find the workers it needs to handle a sharp jump in business. Job fairs run by airline Emirates attract fewer applicants in the U.S. than in other countries. Truck-stop operator Pilot Flying J says job postings don't elicit many more applicants than they did when the unemployment rate was below 5%.I read this and I ask myself why Krugman would think you or I an idiot for giving any credence to what Narayana is talking about? Or how about this:

Matching people with available jobs is always difficult after a recession as the economy remakes itself. But Labor Department data suggest the disconnect is particularly acute this time around. Since the economy bottomed out in mid-2009, the number of job openings has risen more than twice as fast as actual hires, a gap that didn't appear until much later in the last recovery. The disparity is most notable in manufacturing, which has had among the biggest increases in openings. But it is also appearing in other areas, such as business services, education and health care.

Hmm....that "Stuck in the Middle" figure sure looks like a negative aggregate demand shock alright. Or how about the next figure? How can it be that firms (not the government, you will notice) are having trouble filling their openings? Where does this show up in Krugman's IS-LM model, I wonder? Just asking.

Hmm....that "Stuck in the Middle" figure sure looks like a negative aggregate demand shock alright. Or how about the next figure? How can it be that firms (not the government, you will notice) are having trouble filling their openings? Where does this show up in Krugman's IS-LM model, I wonder? Just asking.Here is some more stuff: America's Strongest Job Markets. But of course, it should not be possible to rank domestic job markets in this manner...it's aggregate demand, stupid.

What am I missing here? Is there a legitimate debate to be had, or not? Krugman appears to think not. He is acting more like someone who wants to stifle debate, rather than promote it.

Caveat emptor, I guess.

Sunday, September 26, 2010

Recession, Fed Policy, and Locusts

George Selgin is renowned for his work in monetary theory and history, so when he speaks, he deserves to be listened to: Recession, Fed Policy, and Locusts. (I thank one of my blog visitors for drawing my attention to this article).

I have only a quibble to offer. Selgin remarks that the unemployment rate in the 1870s depression never exceeded 8%. My hunch is that a given rate of unemployment 100 years ago would have imposed much more economic hardship than an identical rate today. (In particular, people are wealthier today, making unemployment more affordable). Also, I am wondering whether the numbers are strictly comparable? I presume that conventions of today's Labor Force Survey were not in place back then. Does anybody out there know?

I have only a quibble to offer. Selgin remarks that the unemployment rate in the 1870s depression never exceeded 8%. My hunch is that a given rate of unemployment 100 years ago would have imposed much more economic hardship than an identical rate today. (In particular, people are wealthier today, making unemployment more affordable). Also, I am wondering whether the numbers are strictly comparable? I presume that conventions of today's Labor Force Survey were not in place back then. Does anybody out there know?

Thursday, September 23, 2010

What is Clear, and Not So Clear, About Fed Policy

I want to comment on some of the reactions I've been reading about lately concerning the Fed's recent policy statement. The full text of the statement can be found here: FOMC September 21, 2010. Here is the last paragraph:

Evidently, the Fed is creating some confusion for the markets. This quote from that article essentially sums it up:

Depending on whom you asked, the central bank either said too much, too little or said it poorly...

Well, the Fed can be annoying at times, I guess. It would be nice if the next time it would say neither too much, nor too little, and--of course--to say all it is saying (and not saying) much more clearly!

But kidding aside, is there a legitimate complaint here? Maybe. What I thought I would do is to list in my own mind the things I think are more and less clear, and then maybe talk about whether any lack of transparency (if it exists) really matters. (Note: I am writing this on the fly, so I'm not really sure where this is going to end up).

What is clear

First, although the Fed has no explicit long-run inflation target (something I believe should be rectified), it's implicit target is widely viewed to be around 2%. Of course, inflation fluctuates around this target and normally, this short-run behavior is of no great concern. The Fed does appear, however, to go on alert when it detects what might be the beginning of an upward or downward trend in the inflation rate (away from the 2% target).

Second, inflation is currently running at around 1% and the short-run recent trend (if it is indeed a trend) is pointing in the downward direction. This event, in and of itself, might normally elicit only a modest concern. But combined with an economy presently weaker than expected, the concern is now heightened. And, in particular, the worry at present is the risk of a Japanese style deflation (a "deflation trap" in the minds of some, though I'm not even sure if such a thing exists).

Third, it seems clear that this risk is presently judged to be "small." But small is not the same thing as zero. Accordingly, the Fed has judged it prudent to issue a contingency plan (note the big IF in the FOMC statement quoted above). You might recall that not too long ago, the Fed was more concerned with another part of its contingency plan (the so-called exit strategy, designed to mitigate inflation fears following the massive expansion in its balance sheet).

Fourth, it seems clear that the Fed stands prepared to "do whatever it takes" to prevent inflation from trending downward any further. (It is also committed to keep inflation reigned in, should we find ourselves on the other side of the inflation target--again, this is the much talked about exit strategy).

What is less clear

The recent FOMC statement did not, however, delve into the details of what tactics the Fed would employ in the event of undesirably low inflation. On the other hand, the Fed has given us a pretty good hint at how it might proceed in its earlier statement: FOMC August 10, 2010; i.e.,

The Committee will continue to monitor the economic outlook and financial developments and is prepared to provide additional accommodation if needed to support the economic recovery and to return inflation, over time, to levels consistent with its mandate.One reaction to this statement can be found here: Fed's Hint of Further Easing Leaves Wall Street Guessing.

Evidently, the Fed is creating some confusion for the markets. This quote from that article essentially sums it up:

Depending on whom you asked, the central bank either said too much, too little or said it poorly...

Well, the Fed can be annoying at times, I guess. It would be nice if the next time it would say neither too much, nor too little, and--of course--to say all it is saying (and not saying) much more clearly!

But kidding aside, is there a legitimate complaint here? Maybe. What I thought I would do is to list in my own mind the things I think are more and less clear, and then maybe talk about whether any lack of transparency (if it exists) really matters. (Note: I am writing this on the fly, so I'm not really sure where this is going to end up).

What is clear

First, although the Fed has no explicit long-run inflation target (something I believe should be rectified), it's implicit target is widely viewed to be around 2%. Of course, inflation fluctuates around this target and normally, this short-run behavior is of no great concern. The Fed does appear, however, to go on alert when it detects what might be the beginning of an upward or downward trend in the inflation rate (away from the 2% target).

Second, inflation is currently running at around 1% and the short-run recent trend (if it is indeed a trend) is pointing in the downward direction. This event, in and of itself, might normally elicit only a modest concern. But combined with an economy presently weaker than expected, the concern is now heightened. And, in particular, the worry at present is the risk of a Japanese style deflation (a "deflation trap" in the minds of some, though I'm not even sure if such a thing exists).

Third, it seems clear that this risk is presently judged to be "small." But small is not the same thing as zero. Accordingly, the Fed has judged it prudent to issue a contingency plan (note the big IF in the FOMC statement quoted above). You might recall that not too long ago, the Fed was more concerned with another part of its contingency plan (the so-called exit strategy, designed to mitigate inflation fears following the massive expansion in its balance sheet).

Fourth, it seems clear that the Fed stands prepared to "do whatever it takes" to prevent inflation from trending downward any further. (It is also committed to keep inflation reigned in, should we find ourselves on the other side of the inflation target--again, this is the much talked about exit strategy).

What is less clear

The recent FOMC statement did not, however, delve into the details of what tactics the Fed would employ in the event of undesirably low inflation. On the other hand, the Fed has given us a pretty good hint at how it might proceed in its earlier statement: FOMC August 10, 2010; i.e.,

To help support the economic recovery in a context of price stability, the Committee will keep constant the Federal Reserve's holdings of securities at their current level by reinvesting principal payments from agency debt and agency mortgage-backed securities in longer-term Treasury securities. The Committee will continue to roll over the Federal Reserve's holdings of Treasury securities as they mature.

In short, the Fed's going to do what it always does when it wants to loosen policy: purchase assets in exchange for newly created money. Which assets? Not short term treasuries--their yields are close to zero. No, it will almost surely include longer dated treasuries, whose yields are currently in the 2.5% range.

There remains some uncertainty in terms of how such a loosening might be implemented over time. A good bet, in my view, would be a state-contingent sequence of purchases, with the quantities purchased depending on how output and inflation evolve over time. The policy rule might take a form like this:

Asset Purchase Rule: Bt - Bt-1 = f ( πt - π, ... )

where the left-hand-side denotes the size of the desired bond purchase (sale, if negative) as a decreasing function of the inflation gap (and possibly other things).

What is not so clear

What if they do all that and it turns out not to be working? In particular, suppose that inflation continues to trend downward as yields on long dated treasuries approach zero? Then what?

Well, there really aren't a lot of options. If the Fed wants to talk inflation up and back its talk with action, it will have to expand the set of securities it is willing to purchase. This much seems clear enough (to me, at least). The only question, in this event, is which securities? (Maybe this is what upsets Wall Street traders, because they would like to know which securities to long and short? If so, they should look on bright side of this opacity: they can continue to blame the Fed for their trading losses).

Now, let's see. Additional MBS purchases are a distinct possibility. Another possibility might be purchases of state and municipal bonds. Of course, moving along this branch of action raises additional questions. High grade or low grade assets, or both? Should the Fed discount a junk municipal bond and, if so, at what rate? But perhaps I am getting ahead of myself. The Fed (Ben Bernanke, in particular)--and indeed, even the Treasury--have both expressed reluctance at the idea of purchasing low-level government debt; e.g., see here: Fed Limited in Ability to Buy Muni Bonds. (Note: "ability" should be properly be replaced with "willingness," I think. And I'm not sure whether this alleged limited ability to buy necessarily rules out an ability to accept these objects as collateral. I will have to look into this).

What is downright blurry

In the event that the economy finds itself in an undesirable deflation dynamic, will any of what I described above actually work? Is this a question that should even be raised in public? (I ask, in part, because there are some people who believe that the Fed should not even have raised the possibility of deflation in the first place, for fear that it would create a self-fulfilling prophesy.)

If we ever arrive in such a world, it will indeed be a strange one. After all, what sort of central bank, with its power to create money "out of thin air," is powerless to affect nominal variables? The Reserve Bank of Zimbabwe appears to have had little difficulty in creating inflation (Note: the hyperinflation in Zimbabwe ended on April 12, 2009. Note too that the Zimbabwean currency no longer exists; see here).

I'm not entirely sure what happened in Zimbabwe, but let me guess: Their fiscal authority used the central bank to create money that was then spent on goods and services that were largely consumed (someone correct me if I am wrong). Money created and used in this manner is never retired and generates no income (income that could, for example, be used to finance future purchases of goods, or retire the money stock). Yes, I think we can all be fairly confident that fiscal authorities have the power to create inflation (and expectations of inflation).

In the U.S., however, the Fed is independent of the fiscal authority (at least, it likes to think it is). When the Fed creates new money, it is restricted to inject it into the economy via asset purchases only (normally U.S. treasury debt, or other high-grade securities). How might this restriction matter?

Here is one possibility. Imagine that, for some reason, everyone expects a persistent deflation of, say, 2%. Moreover, imagine that the "natural" (real) rate of interest on high-grade securities is also 2%. Then, if the Fed targets the nominal interest rate anywhere above zero, the real rate of interest will be "too high" (depressing aggregate demand). The Fed is compelled to cut its interest rate to zero. A no-arbitrage-condition implies that the nominal yields on similar assets will also fall close to zero. In this event, swaps of zero interest money for zero interest securities is not likely to have any effect at all.

The Fed could, however, try to purchase higher-risk asset classes. The yields on these assets are far above zero, reflecting the probability of default, one would guess. Now, these assets will either pay off or not. If they pay off, the Fed is obliged to remit this profit to the Treasury (hence, the Fed has no control over how this profit is ultimately spent). If they don't pay off, the Fed will take a loss. Well, not a loss exactly. The Fed might (in principle, at least) simply keep the nonperforming loan on its books as an asset that expected to pay off sometime in the infinite future. In short, it becomes a perpetual zero interest loan--in effect, a lump-sum transfer of cash into the economy.

I haven't thought through the logic entirely yet, but it appears that out of these two scenarios, the expectation of outright defaults would resemble a series of lump-sum cash injections into the economy; something that we are fairly confident would generate inflationary pressure (it works well in our models, at least). On the other hand, if the assets are largely expected pay off, with the profits remitted to the Treasury, the inflationary consequences will depend on the subsequent actions of the fiscal authority.

So, at the end of the day, the Fed acting on its own, and under the current institutional framework, may not even have the capacity to influence nominal variables in some (low probability) states of the world. A commitment to an inflation target would, in this case appear to require explicit language explaining the joint monetary/fiscal behavior deemed necessary to achieve the stated goal.

I'm not holding my breath waiting for this language to appear anytime soon, primarily because I think that the risk of this scenario is still judged to be relatively small. But, we shall see.

There remains some uncertainty in terms of how such a loosening might be implemented over time. A good bet, in my view, would be a state-contingent sequence of purchases, with the quantities purchased depending on how output and inflation evolve over time. The policy rule might take a form like this:

Asset Purchase Rule: Bt - Bt-1 = f ( πt - π, ... )

where the left-hand-side denotes the size of the desired bond purchase (sale, if negative) as a decreasing function of the inflation gap (and possibly other things).

What is not so clear

What if they do all that and it turns out not to be working? In particular, suppose that inflation continues to trend downward as yields on long dated treasuries approach zero? Then what?

Well, there really aren't a lot of options. If the Fed wants to talk inflation up and back its talk with action, it will have to expand the set of securities it is willing to purchase. This much seems clear enough (to me, at least). The only question, in this event, is which securities? (Maybe this is what upsets Wall Street traders, because they would like to know which securities to long and short? If so, they should look on bright side of this opacity: they can continue to blame the Fed for their trading losses).

Now, let's see. Additional MBS purchases are a distinct possibility. Another possibility might be purchases of state and municipal bonds. Of course, moving along this branch of action raises additional questions. High grade or low grade assets, or both? Should the Fed discount a junk municipal bond and, if so, at what rate? But perhaps I am getting ahead of myself. The Fed (Ben Bernanke, in particular)--and indeed, even the Treasury--have both expressed reluctance at the idea of purchasing low-level government debt; e.g., see here: Fed Limited in Ability to Buy Muni Bonds. (Note: "ability" should be properly be replaced with "willingness," I think. And I'm not sure whether this alleged limited ability to buy necessarily rules out an ability to accept these objects as collateral. I will have to look into this).

What is downright blurry

In the event that the economy finds itself in an undesirable deflation dynamic, will any of what I described above actually work? Is this a question that should even be raised in public? (I ask, in part, because there are some people who believe that the Fed should not even have raised the possibility of deflation in the first place, for fear that it would create a self-fulfilling prophesy.)

If we ever arrive in such a world, it will indeed be a strange one. After all, what sort of central bank, with its power to create money "out of thin air," is powerless to affect nominal variables? The Reserve Bank of Zimbabwe appears to have had little difficulty in creating inflation (Note: the hyperinflation in Zimbabwe ended on April 12, 2009. Note too that the Zimbabwean currency no longer exists; see here).

I'm not entirely sure what happened in Zimbabwe, but let me guess: Their fiscal authority used the central bank to create money that was then spent on goods and services that were largely consumed (someone correct me if I am wrong). Money created and used in this manner is never retired and generates no income (income that could, for example, be used to finance future purchases of goods, or retire the money stock). Yes, I think we can all be fairly confident that fiscal authorities have the power to create inflation (and expectations of inflation).

In the U.S., however, the Fed is independent of the fiscal authority (at least, it likes to think it is). When the Fed creates new money, it is restricted to inject it into the economy via asset purchases only (normally U.S. treasury debt, or other high-grade securities). How might this restriction matter?

Here is one possibility. Imagine that, for some reason, everyone expects a persistent deflation of, say, 2%. Moreover, imagine that the "natural" (real) rate of interest on high-grade securities is also 2%. Then, if the Fed targets the nominal interest rate anywhere above zero, the real rate of interest will be "too high" (depressing aggregate demand). The Fed is compelled to cut its interest rate to zero. A no-arbitrage-condition implies that the nominal yields on similar assets will also fall close to zero. In this event, swaps of zero interest money for zero interest securities is not likely to have any effect at all.

The Fed could, however, try to purchase higher-risk asset classes. The yields on these assets are far above zero, reflecting the probability of default, one would guess. Now, these assets will either pay off or not. If they pay off, the Fed is obliged to remit this profit to the Treasury (hence, the Fed has no control over how this profit is ultimately spent). If they don't pay off, the Fed will take a loss. Well, not a loss exactly. The Fed might (in principle, at least) simply keep the nonperforming loan on its books as an asset that expected to pay off sometime in the infinite future. In short, it becomes a perpetual zero interest loan--in effect, a lump-sum transfer of cash into the economy.

I haven't thought through the logic entirely yet, but it appears that out of these two scenarios, the expectation of outright defaults would resemble a series of lump-sum cash injections into the economy; something that we are fairly confident would generate inflationary pressure (it works well in our models, at least). On the other hand, if the assets are largely expected pay off, with the profits remitted to the Treasury, the inflationary consequences will depend on the subsequent actions of the fiscal authority.

So, at the end of the day, the Fed acting on its own, and under the current institutional framework, may not even have the capacity to influence nominal variables in some (low probability) states of the world. A commitment to an inflation target would, in this case appear to require explicit language explaining the joint monetary/fiscal behavior deemed necessary to achieve the stated goal.

I'm not holding my breath waiting for this language to appear anytime soon, primarily because I think that the risk of this scenario is still judged to be relatively small. But, we shall see.

Monday, September 20, 2010

Tyler Cowen's Happy Face Inflation Policy

Here is the basic idea, as I understand it. The future is dark and uncertain; there is no sound basis for making long-horizon forecasts. This opens a door for psychology. Communities are now prone to psychologically-inspired waves of optimism and pessimism ("animal spirits," to use Keynes' colorful phrase). Since current investment demand primarily runs off of long-horizon forecasts (relating to the expected return to future capital), these animal spirits lead to large fluctuations in "aggregate demand" via investment spending. Things are even worse in a monetary economy, as the existence of cash facilitates a psychologically-inspired "flight to safety" that, while perhaps individually rational, contributes to a socially irrational contraction in aggregate demand. The contraction in aggregate demand means lower sales volumes, so firms lay off workers, who are now unemployed. As unemployed workers generate no wage income, they cut back on purchases, which contributes further to lower demand. Firms are induced to cut prices, which leads to deflation. As debt is nominally denominated (not indexed to inflation), the deflation raises the real debt burden of indebted households and firms. Debt renegotiation is possible, but the process is costly and slow. The upshot is a wave of bankruptcies that contributes to the depressed business climate.

The "social problem," in a nutshell, concerns the dynamics of mass psychology in a free market system. In a free market, individuals are (by definition) free to make their own economic decisions. Naturally, they do so without full regard of how their individual decisions might influence aggregate outcomes (an individual, after all, is tiny relative to the community). People value their economic liberty for a good reason, but liberty comes at a cost. The cost is that individuals may not always coordinate their decisions in a socially desirable manner (for example, in noncooperative games, Nash equilibria are generically suboptimal).

Well, if that is the problem, then the solution is straightforward; in principle, at least. Unlike individuals, the government is a large player. If we are collectively depressed for no good reason, then why not have the government bring on some good cheer? Insufficient demand is easily rectified by more government spending and a loose monetary policy. Inflation (some inflation, at least) is good. It gets people to spend their money (it would otherwise lose purchasing power). As people spend, sales volumes rise, profit margins rise, and firms are induced to employ more workers.

It is a seductive argument. And on the surface, it is hard to see what, if anything, is wrong with it. At least one or two prominent bloggers are apt to call you "stupid" for not seeing it as a self-evident truth. Let's not be bullied by these over-inflated egos and try to think this through ourselves.

The first thing we should realize is that the argument may have some merit. It may even be completely true (in the sense that the described theoretical forces provide a good approximation for quantitatively important forces that actually operate in the economy). On the other hand, it may not be the whole story. Heck, it may even be false. (I realize that this is not an appealing message for those who find comfort in religion, but I am a social scientist, not a preacher).

Let's start with psychology. There is no question that people get emotional and that emotions can sometimes color decision-making. Accepting this does not, however, lead immediately to the conclusion that emotional decision-making is individually or collectively irrational. If I see a bear on my running trail, I freak out and run away (this actually happened to me, and looking back, I think I acted in a perfectly rational manner!). And from a Darwinian perspective, it is hard to see how a propensity for collective irrationality has led to our flourishing modern day civilization (although, I have to admit that wars are crazy and that Collapse is always a possibility).

True, market optimism appears to wax and wane, but so what? It is possible, even if one does not find it entirely plausible, that these undulations constitute, at least in part, waves of rational optimism and rational pessimism. I have a simple model here that formalizes this view. In that model, an increase in government spending, even in a liquidity trap scenario, is not the correct policy. (The model replicates many of the key properties of a standard New Keynesian model, so it would be hard to discount the model on the basis of its predictions).

The "deficit of optimism" hypothesis espoused by Cowen and others has other potential shortcomings. Among other things, it tends to ignore what transpired just prior to the collapse in confidence. An "Austrian" view is that an artificially low interest rate (via Fed policy earlier in the decade) created an unsustainable over build in capital. The present depression is more like a coming to your senses after a bout of irrational optimism. An alternative hypothesis that generates an observationally equivalent rational expectations outcome can be found in this (unduly neglected) paper by Joseph Zeira: Informational Overshooting, Booms and Crashes.

I wonder, as well, what direct evidence supports the notion of depressed "animal spirits?" In this post, I took a look at the short and long-horizon forecasts (for real GDP growth) in the Philadelphia Survey of Professional Forecasters. Call me stupid if you want, but I don't see long-horizon forecasts jumping around all over the place. Indeed, the long-horizon forecast displays a remarkable stability even through the worst parts of the financial crisis. It is interesting to note that these forecasts imply a decline in what an econometrician would measure as "potential GDP." But if the prior boom was simply a "bubble" (as many in this camp are inclined to argue) is there any reason to want a return to that "false" level of potential? You can't have your cake and eat it too: either we had a bubble and potential is now lower, or there was no bubble and potential remains unchanged.

But what about the high rate of unemployment? Does this not constitute evidence of a "deficit of optimism?" Is it not evidence of sticky wages and an economy wide lack of demand? I have spoken elsewhere about the sticky wage hypothesis; see here. Moreover, I am not so sure about the "negative aggregate demand shock hypothesis" affecting the labor market when I look at data like this. There's lots of interesting stuff happening at the sectoral level that might account for a lot of what we are experiencing; see also this post by Steve Williamson.

I have argued elsewhere that a good case can be made for redistributive policies that help individuals smooth their living standards across different contingencies. Public works sound like a good idea if they can be justified in NPV terms (though, these interventions are typically sectoral in nature). Extending UI through a deep recession seems like a sensible idea--but please don't be surprised if this leads to higher unemployment rates and extended unemployment durations--and then argue that this is evidence of insufficient demand!

I am, however, deeply skeptical of Tyler Cowen's proposed remedy of higher inflation; or, more precisely, the happy expectation of higher inflation. Don't get me wrong--I think that an unexpected disinflation (or deflation) is likely to be harmful in the short-run (because debt is nominally denominated). The disinflation we have been witnessing has, in my view, little to do with a psychologically driven short-fall in aggregate demand and has a lot to do with an entirely rational increase in the world demand for U.S. government money/debt. Keeping inflation expectations targeted at 2 or 3 percent (or 1 or 0, for that matter) seems entirely appropriate. But there is little reason, in my view, to expect such a policy to "cure" unemployment.

These are, of course, my own views and not necessarily those of the Fed (my current employer). Indeed, as Cowen points out, my current boss appears to have expressed a very different opinion in the past; see here. I don't agree with Bernanke on this point (I visited the BOJ in 2002 and came to different conclusions), and I feel privileged to work at an institution that encourages different ways of thinking about things. Having said this, I have to disagree with Mr. Cowen's portrayal of Chairman Bernanke's current position:

In failing to push harder for monetary expansion, is Mr. Bernanke a wise and prudent guardian of the limited discretionary powers of the Fed? Or is he acting like a too-hesitant bureaucrat, afraid to fail and take the blame when he should be gunning for success?(I wonder what the Ron Paul supporters must be thinking about that first statement?). I think that the Chairman has made his views pretty clear here: Deflation: Making Sure "It" Doesn't Happen Here. In a nutshell, I do not think that he views Japan as a relevant scenario for the U.S.; see also his Jackson Hole speech:

A rather different type of policy option, which has been proposed by a number of economists, would have the Committee increase its medium-term inflation goals above levels consistent with price stability. I see no support for this option on the FOMC. Conceivably, such a step might make sense in a situation in which a prolonged period of deflation had greatly weakened the confidence of the public in the ability of the central bank to achieve price stability, so that drastic measures were required to shift expectations. Also, in such a situation, higher inflation for a time, by compensating for the prior period of deflation, could help return the price level to what was expected by people who signed long-term contracts, such as debt contracts, before the deflation began.

However, such a strategy is inappropriate for the United States in current circumstances. Inflation expectations appear reasonably well-anchored, and both inflation expectations and actual inflation remain within a range consistent with price stability. In this context, raising the inflation objective would likely entail much greater costs than benefits. Inflation would be higher and probably more volatile under such a policy, undermining confidence and the ability of firms and households to make longer-term plans, while squandering the Fed's hard-won inflation credibility. Inflation expectations would also likely become significantly less stable, and risk premiums in asset markets--including inflation risk premiums--would rise. The combination of increased uncertainty for households and businesses, higher risk premiums in financial markets, and the potential for destabilizing movements in commodity and currency markets would likely overwhelm any benefits arising from this strategy.

In short, I see no inconsistency here in terms of his earlier policy recommendations for Japan (which I think were wrong) and the policy that he is currently advocating.

Note: I apologize if my thoughts above appear a little scattered. But I was hit rather severely on the head with a soccer ball yesterday!

Thursday, September 16, 2010

Uncertainty over New Deals

Lot's of chatter these days about what role the uncertainty over future policy regimes is playing in holding back a complete economic recovery. On the one side, we have the usual suspects claiming that the problem has little, if anything, to do with policy uncertainty. Instead, it is a lack of "aggregate demand." Mark Thoma provides a link to an interesting study here that appears to support this hypothesis--on the surface, at least.

The study highlights the fact that small businesses are citing a lack of sales volume as their main source of trouble. Well, sure. But it's not immediately obvious what this micro data tells us about the empirical relevance of the theory of "effective demand failure" in the current climate. Small businesses living in an intersectoral real business cycle model (a la Long and Plosser, JPE 1983) are likely to report similar things in the event of a large negative shock to an important sector of the economy (like the residential investment sector). If I'm a supplier of home furnishings, I'm going to cite a lack of demand for my product. But does this necessarily mean that the macro problem is a lack of aggregate demand? Possibly--but not necessarily.

In an earlier post, I entertained the idea of investment demand falling off the cliff in response to fundamentally bad news relating to the future return to capital spending; see here. I still think there is some merit in this idea, though the data I presented here has led me to re-think this position. I could be wrong, but I think this data presents a similar difficulty for standard Keynesian interpretations of investment spending collapse. In particular, the survey data I cite shows that long-horizon forecasts of real GDP growth remain resiliently optimistic throughout the worst parts of the recession. (Presumably, it is the long-horizon that bears most forcefully on current planned investment decisions). The same data shows an increasing amount of "uncertainty" (or disagreement) over forecasts. Of course, the data does not tell us the source of this uncertainty; but it seems reasonable to suppose that at least some of it is being generated by the government and the Fed (Disclaimer: the views expressed here are obviously my own!)

With respect to this uncertainty theme, a reader of my earlier post provided an interesting link Regime Uncertainty: Reports Keep Coming In. The author of this is one Robert Higgs (never heard of him before), who has also written this interesting paper: Regime Uncertainty: Why the Great Depression Lasted So Long and Why Prosperity Resumed After the War. I'm not sure what you think of all this, but maybe the guy has a valid point.

Oddly enough, Brad DeLong provides some support for this hypothesis here: The New Deal: Lessons for Today. What do I mean by this? Well, let me quote:

Drawing lessons from the New Deal for the Great Depression requires, first, and understanding what the New Deal was. It was a gumbo: FDR took everything that was on the kitchen shelf and threw it into the pot on March 4, 1933 and then began stirring.He quotes FDR himself as saying:

The country needs and, unless I mistake its temper, the country demands bold, persistent experimentation. It is common sense to take a method and try it. If it fails, admit it frankly and try another. But above all, try something.Now, whether you agree with FDR's approach here or not, I think you'd be hard pressed to argue that it did not contribute to a heightened degree of uncertainty over the likely future path of policy interventions. But clearly, something had to be done; so perhaps this approach was defensible under the circumstances.

Or was it? What sort of "common sense" was FDR referring to anyway? The U.S. economy had experienced severe economic contractions prior to 1930, the most recent in the early 1920s. While severe and distressing for many people, the economy always recovered on its own (the size of the federal government in those years was tiny in comparison to today). What was it about the contraction in 1930-33 that made it so much more different than before? Was there any reason to believe at that time that the economy would not recover on its own as it did before, without anything resembling a New Deal intervention? Why did the contraction of that period result in a "lost decade?" Is it really crazy to suppose that FDR's "gumbo soup" approach may have prolonged the misery of that decade? I honestly do not know the answer to these questions, but I think they should be taken seriously.

Many people appear to buy into the standard myth of an established and stubborn free-market orthodoxy, led by Herbert Hoover, ready to drive the U.S. economy to hell--until FDR saved the free world with his New Deal. My own reading of that period in American history has left me with a different perspective (my views are still evolving as I continue to read, of course).

The economic orthodoxy of the time was largely persuaded by the benefits of countercyclical public works (see, Fabricating the Keynesian Revolution, by David Laidler). And Herbert Hoover was (initially, at least) a big proponent of public works (remember, he served as Secretary of Commerce from 1920-28). He described himself as a "progressive" and a "reformer" and in his writings, he criticized laissez-faire economics. His response during the great contraction was to introduce his own New Deal; see here.

Naturally, Herbert Hoover's New Deal had many critics. Not the least of these were the Democrats in Congress (who were in a majority at that time), led by FDR himself. I am still reading through the history of that time (one needs to check several sources, since there appear to be conflicting reports and interpretations). But it seems clear enough that there was quite a bit of political wrangling going on--very much like what we see today, in fact. The Democrats at that time (much like the Republicans today) apparently did everything they could to stonewall the President and his policies. But at the end of the day, many of FDR's New Deal policies were lifted from Hoover's. Consider, in particular, this quote from one of FDR's early advisers (Raymond Moley, writing in Newsweek, June 14, 1948):

When we all burst into Washington...we found every essential idea (of the New Deal) enacted in the 100-day Congress in the Hoover administration itself. The essentials of the NRA, the PWA, the emergency relief setup were all there. Even the AAA was known to the Department of Agriculture. Only the TVA and the Securities Act was drawn from other sources. The RFC, probably the greatest recovery agency, was of course a Hoover measure, passed long before the inauguration.Of course, the U.S. economy continued to collapse despite Hoover's New Deal. Does this not require some explaining? The most tumultuous events appear to coincide with the period between Hoover's election loss and FDR's official appointment to office. Consider this quote from here:

The election brought hope to many Americans in the autumn of 1932.

But Roosevelt did not become president until March 1933, four months after the election. And those months saw the American economy fall to its lowest level in the history of the nation. President Hoover tried to arrange a world economic conference. And he called on President-elect Roosevelt to join him in making conservative statements in support of business.

Roosevelt refused. He did not think it was correct to begin acting like a president until he actually became the head of government. He did not want to tie himself to policies that the voters had just rejected. Congress, controlled by Democrats, also refused to help Hoover.

It was a strange period, a season of uncertainty and anger. The Economic Depression was worse than ever. The lines of people waiting for food were longer than before. Angry mobs of farmers were gathering in the countryside. And the politicians in Washington seemed unable to work together to end the crisis.

Hoover said: "We are at the end of our rope. There is nothing more we can do." And across the country, Americans waited -- worried, uncertain, afraid. What would the new president do?

Whatever one's political philosophy, I think that we might all agree that uncertainty over policy regimes has played a role in past depressions. And it may very well be playing a role in depressing the current recovery.

Tuesday, September 14, 2010

Cyclical Variation in Short and Long Run Expectations

A little while ago, (the mad, mad I say) Nick Rowe of WCI posted this: The Bond Bubble, and Why We Should Be Worried About It. As with most of Nick's observations, it got me thinking a bit.

Both Nick and I agree that investors appear to be substituting out of private securities and into government securities (in particular, USD and US treasuries). We appear to differ on the underlying cause of this behavior.

Nick takes the bubble and its behavior as exogenous. There is a growing bubble in money/bonds, which is drawing resources away from private capital investment. In a comment on Nick's post, I suggested an alternative interpretation. I take expectations over the future return to capital as exogenous and interpret the bubble asset as a socially beneficial alternative store of value (in theory, such bubbles can mitigate the adverse consequences of a dynamic inefficiency).

The type of model I have in mind can be found here. In that model, money (bonds) and capital compete as a store of value in the wealth portfolios of individuals. Assuming risk neutrality and diminishing returns to capital investment, a no-arbitrage-condition equates the expected marginal product of capital to the expected real rate of return on money. I then define "good news" as information that leads to an upward revision in the forecast of capital return; "bad news" is defined conversely. I argued that a bad news event (or a series of bad news events) would cause rational downward revisions in the forecasted return to future capital, thereby depressing capital investment and stock prices, and causing a flow of resources into government money/bonds. There would be "surprise" declines in the price-level (reflecting the increase in demand for money). The resulting behavior looks like an exogenous increase in the demand for government securities, but this is the wrong interpretation.

In a subsequent discussion, Simon van Norden asked me to explain what evidence I had to support the notion that shocks to expectations (over future capital return) varied significantly and at high frequency. These are the type of impolite questions that I think need to be asked. I replied, rather lamely I think, that these expectations were difficult to measure (except perhaps, indirectly via asset prices). I think I even stooped to the time-honored tradition of citing the importance that our predecessors attached to the hypothesis (think Keynes, Pigou, Marshall, and so on, back in time). Simon suggested that I look at the Federal Reserve Bank of Philadelphia's Survey of Professional Forecasters. Thanks, Simon!

I am kind of leery of this data, as the forecasts of professional forecasters are not necessarily the same thing as the forecasts of businessmen in charge of making multimillion dollar investments. Moreover, the survey does not ask about forecasts over the return to capital...the closest measure is future real GDP growth. But what the heck...some data is better than no data.

And the data looks kind of interesting. In Figure 1, I plot the average (over all forecasters) expected growth rate over five periods: the current quarter, one quarter ahead, ..., up to four quarters ahead. (Click on the figure to enlarge). I do this for each quarter, beginning with 2007:4 and ending with 2010:2. The dashed line measures actual (revised) real GDP growth. Let me summarize some facts about this data that I find interesting.

FACT 1: Short-run forecasts are much more volatile than long-run forecasts.

Personally, I find the resiliency in the year-ahead forecasts rather remarkable. Even in the depths of the financial crisis, these professional forecasters were forecasting a return to normal rates of growth within a year or so. Do they run the same canned VAR models to come up with these forecasts? I wonder whether businessmen in charge of capital budgets were as optimistic as these professional forecasters in the fourth quarter of 2008?

FACT 2: The recent recession appears to be associated with a persistent (possibly permanent) decline in potential GDP.

An expected return to "potential" GDP would require year-ahead forecasts to exceed 2% per annum coming out of the recession. This does not appear to be the case; at least, not so far.

I wonder how Pigou and Keynes would have reacted to this data. If I understand their views correctly, it is precisely the long-horizon that is subject to the psychology of animal spirits. And because capital investment today runs largely off of long-horizon forecasts, this is what makes investment so volatile. This view (which is related to my own) does not seem to be supported by this data.

On the other hand, even changes in short-horizon forecasts can induce changes in asset prices. And to the extent that assets are used as collateral in lending, a decline in asset prices may depress investment spending through the familiar accelerator. (I have written a model, with my SFU colleague Fernando Martin, that is being extended in this manner).

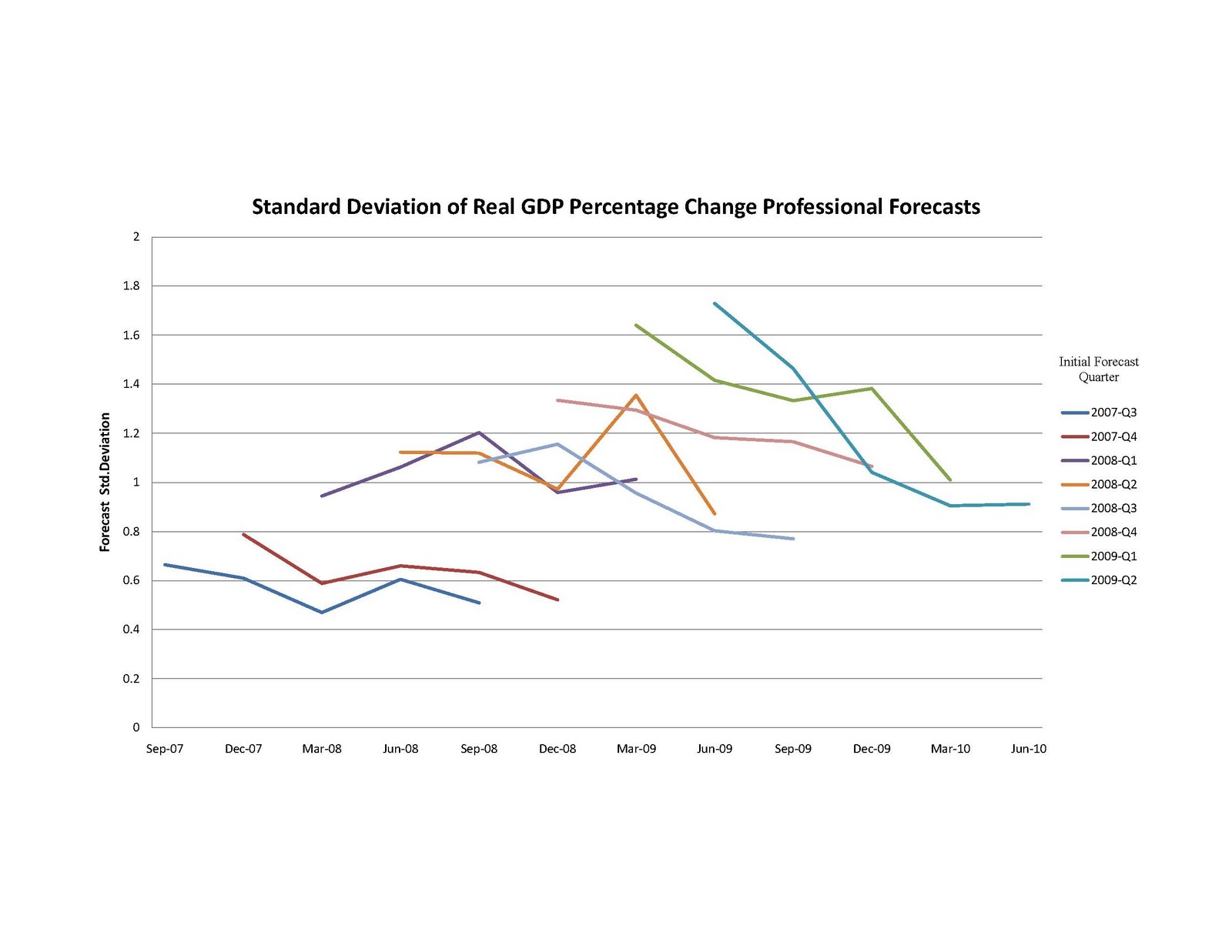

It is also of some interest to explore some higher moments associated with these growth forecasts. In Figure 2, I plot the standard deviation of forecasts (across forecasters) in each quarter and at each horizon. I interpret this standard deviation as a measure of "uncertainty."

Figure 2 suggests that the uncertainty over long-horizon growth increased substantially since the beginning of the recession and continues to remain high. In a nutshell, these forecasters are expecting a return to 2% growth in the long-horizon, but there appears to be much more uncertainty among these forecasters about the prospect of such an event.

It is also curious to see how "uncertainty" over the short-horizon increases dramatically. I view this as some evidence against Nick's hypothesis and in favor of my own (extended to include higher moments, of course). The emerging bond bubble is the consequence of increasing uncertainty over short and long term capital returns; this same uncertainty is contributing to depressed capital expenditure.

In short, I think that Nick might have the direction of causality ass-backwards.

* I thank Constanza Liborio for gathering and plotting this data.

Both Nick and I agree that investors appear to be substituting out of private securities and into government securities (in particular, USD and US treasuries). We appear to differ on the underlying cause of this behavior.

Nick takes the bubble and its behavior as exogenous. There is a growing bubble in money/bonds, which is drawing resources away from private capital investment. In a comment on Nick's post, I suggested an alternative interpretation. I take expectations over the future return to capital as exogenous and interpret the bubble asset as a socially beneficial alternative store of value (in theory, such bubbles can mitigate the adverse consequences of a dynamic inefficiency).

The type of model I have in mind can be found here. In that model, money (bonds) and capital compete as a store of value in the wealth portfolios of individuals. Assuming risk neutrality and diminishing returns to capital investment, a no-arbitrage-condition equates the expected marginal product of capital to the expected real rate of return on money. I then define "good news" as information that leads to an upward revision in the forecast of capital return; "bad news" is defined conversely. I argued that a bad news event (or a series of bad news events) would cause rational downward revisions in the forecasted return to future capital, thereby depressing capital investment and stock prices, and causing a flow of resources into government money/bonds. There would be "surprise" declines in the price-level (reflecting the increase in demand for money). The resulting behavior looks like an exogenous increase in the demand for government securities, but this is the wrong interpretation.

In a subsequent discussion, Simon van Norden asked me to explain what evidence I had to support the notion that shocks to expectations (over future capital return) varied significantly and at high frequency. These are the type of impolite questions that I think need to be asked. I replied, rather lamely I think, that these expectations were difficult to measure (except perhaps, indirectly via asset prices). I think I even stooped to the time-honored tradition of citing the importance that our predecessors attached to the hypothesis (think Keynes, Pigou, Marshall, and so on, back in time). Simon suggested that I look at the Federal Reserve Bank of Philadelphia's Survey of Professional Forecasters. Thanks, Simon!

I am kind of leery of this data, as the forecasts of professional forecasters are not necessarily the same thing as the forecasts of businessmen in charge of making multimillion dollar investments. Moreover, the survey does not ask about forecasts over the return to capital...the closest measure is future real GDP growth. But what the heck...some data is better than no data.

And the data looks kind of interesting. In Figure 1, I plot the average (over all forecasters) expected growth rate over five periods: the current quarter, one quarter ahead, ..., up to four quarters ahead. (Click on the figure to enlarge). I do this for each quarter, beginning with 2007:4 and ending with 2010:2. The dashed line measures actual (revised) real GDP growth. Let me summarize some facts about this data that I find interesting.

|

| FIGURE 1 |

FACT 1: Short-run forecasts are much more volatile than long-run forecasts.

Personally, I find the resiliency in the year-ahead forecasts rather remarkable. Even in the depths of the financial crisis, these professional forecasters were forecasting a return to normal rates of growth within a year or so. Do they run the same canned VAR models to come up with these forecasts? I wonder whether businessmen in charge of capital budgets were as optimistic as these professional forecasters in the fourth quarter of 2008?

FACT 2: The recent recession appears to be associated with a persistent (possibly permanent) decline in potential GDP.

An expected return to "potential" GDP would require year-ahead forecasts to exceed 2% per annum coming out of the recession. This does not appear to be the case; at least, not so far.

I wonder how Pigou and Keynes would have reacted to this data. If I understand their views correctly, it is precisely the long-horizon that is subject to the psychology of animal spirits. And because capital investment today runs largely off of long-horizon forecasts, this is what makes investment so volatile. This view (which is related to my own) does not seem to be supported by this data.

On the other hand, even changes in short-horizon forecasts can induce changes in asset prices. And to the extent that assets are used as collateral in lending, a decline in asset prices may depress investment spending through the familiar accelerator. (I have written a model, with my SFU colleague Fernando Martin, that is being extended in this manner).

It is also of some interest to explore some higher moments associated with these growth forecasts. In Figure 2, I plot the standard deviation of forecasts (across forecasters) in each quarter and at each horizon. I interpret this standard deviation as a measure of "uncertainty."

|

| FIGURE 2 |

Figure 2 suggests that the uncertainty over long-horizon growth increased substantially since the beginning of the recession and continues to remain high. In a nutshell, these forecasters are expecting a return to 2% growth in the long-horizon, but there appears to be much more uncertainty among these forecasters about the prospect of such an event.

It is also curious to see how "uncertainty" over the short-horizon increases dramatically. I view this as some evidence against Nick's hypothesis and in favor of my own (extended to include higher moments, of course). The emerging bond bubble is the consequence of increasing uncertainty over short and long term capital returns; this same uncertainty is contributing to depressed capital expenditure.

In short, I think that Nick might have the direction of causality ass-backwards.

* I thank Constanza Liborio for gathering and plotting this data.

Friday, September 3, 2010

Tom Sargent Speaks

Arthur J. Rolnick (Director of Research at the Minneapolis Fed, 1985-2010) recently interviewed Thomas J.Sargent on a range of issues, including the criticisms levelled at modern macroeconomic theory. Here is the opening bit, which I found rather amusing:

Modern macroeconomics under attack

Rolnick: You have devoted your professional life to helping construct and teach modern macroeconomics. After the financial crisis that started in 2007, modern macro has been widely attacked as deficient and wrongheaded.

Sargent: Oh. By whom?

Rolnick: For example, by Paul Krugman in the New York Times and Lord Robert Skidelsky in the Economist and elsewhere. You were a visiting professor at Princeton in the spring of 2009. Along with Alan Blinder, Nobuhiro Kiyotaki and Chris Sims, you must have discussed these criticisms with Krugman at the Princeton macro seminar.

Sargent: Yes, I was at Princeton then and attended the macro seminar every week. Nobu, Chris, Alan and others also attended. There were interesting discussions of many aspects of the financial crisis. But the sense was surely not that modern macro needed to be reconstructed. On the contrary, seminar participants were in the business of using the tools of modern macro, especially rational expectations theorizing, to shed light on the financial crisis.

Rolnick: What was Paul Krugman’s opinion about those Princeton macro seminar presentations that advocated modern macro?

Sargent: He did not attend the macro seminar at Princeton when I was there.

Rolnick: Oh.

The entire interview is available here.

Modern macroeconomics under attack

Rolnick: You have devoted your professional life to helping construct and teach modern macroeconomics. After the financial crisis that started in 2007, modern macro has been widely attacked as deficient and wrongheaded.

Sargent: Oh. By whom?

Rolnick: For example, by Paul Krugman in the New York Times and Lord Robert Skidelsky in the Economist and elsewhere. You were a visiting professor at Princeton in the spring of 2009. Along with Alan Blinder, Nobuhiro Kiyotaki and Chris Sims, you must have discussed these criticisms with Krugman at the Princeton macro seminar.

Sargent: Yes, I was at Princeton then and attended the macro seminar every week. Nobu, Chris, Alan and others also attended. There were interesting discussions of many aspects of the financial crisis. But the sense was surely not that modern macro needed to be reconstructed. On the contrary, seminar participants were in the business of using the tools of modern macro, especially rational expectations theorizing, to shed light on the financial crisis.

Rolnick: What was Paul Krugman’s opinion about those Princeton macro seminar presentations that advocated modern macro?

Sargent: He did not attend the macro seminar at Princeton when I was there.

Rolnick: Oh.

The entire interview is available here.

Subscribe to:

Posts (Atom)