Nick Rowe's post on upward-sloping IS curves motivates today's musings. I'm sorry, but what follows is a tad on the wonkish side. It's intended mainly to promote a conversation with Nick. (You can look in if you want, but I'm sure most of you have better things to do on Christmas Eve!).

Consider the Solow growth model. Output (the real GDP) is produced with capital (K) and labor (N) according to a neoclassical aggregate production function Y = F(K,N).

Define y = Y/N (output per worker) and k = K/N (capital-labor ratio). Define f(k) = F(K/N,1). Then y = f(k). That is, output per worker is an increasing function of capital per worker.

If capital and labor are exchanged on competitive markets, then factor prices are equated to their respective marginal products. Let (w,r) denote the real wage and the real rental rate, respectively. Let 0 < a < 1 denote capital's share of income. Then,

[1] w = (1 - a)f(k) and r = af(k)/k

That is, the real wage is an increasing function of the capital-labor ratio (since labor becomes relatively scarce). The real rental rate for capital services is a decreasing function of the capital-labor ratio (since capital becomes relatively abundant).

Now, consider an economy populated by two-period-lived overlapping generations. People enter the economy as youngsters, they become old, and then they exit the economy. The population of young people remains fixed at N over time t = 0,1,2,... The young are each endowed with one unit of labor, which they supply inelastically at the going wage. Hence, N represents labor supply. The young save all their income and consume only when they are old. Saving is used to finance investment, which adds to the future stock of productive capital. For simplicity, assume that capital depreciates fully after it is used in production. (None of the results below are sensitive to these simplifying assumptions).

Since a young person saves his entire wage, the capital stock (per worker) evolves over time as follows:

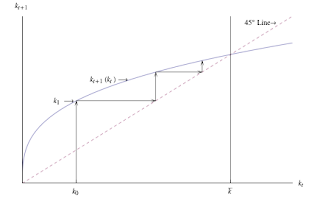

[2] k(t+1) = (1 - a)f(k(t)) for t = 0,1,2,... with k(0) > 0 given (as an initial condition).

The transition dynamics are such that k(t) converges monotonically to a steady-state satisfying k* = (1 - a)f(k*).

The real interest rate at date t in this model is equal to the future (t+1) marginal product of capital (which is proportional to the average product of capital), R(t) = af(k(t+1)) = af((1 -a)y(t) ) / ((1-a)y(t) ).

The IS curve in this model is defined as the locus of real interest rates and output consistent with goods-market-clearing. In the present context:

[3] R(t) = af( (1-a)y(t) )/( (1-a)y(t) ).

Equation [3] describes a conventional downward-sloping IS curve. A higher level of income (because of more abundant capital) increases desired saving, which puts downward pressure on the real interest rate. Conversely, an increase in the real interest rate reduces aggregate demand.

Now, let's consider one of Nick's experiments. Begin in a steady state. Nick considers an exogenous 10% increase in the capital stock. I'll do the opposite experiment and consider a 10% decline.

The capital-labor ratio is now lower. From [1], the effect is to lower the real wage and increase the rental rate. From its depressed level, the real wage increases monotonically back to its steady-state level. From its elevated level, the rental rate declines back to its steady-state level. The real interest rate, in turn, jumps up and then declines back to its steady-state level.

In a competitive economy, these price adjustments reflect the underlying fundamentals. The shock renders capital scarce. Less capital depresses the demand for labor, which is reflected in a lower real wage. Capital scarcity means the the return to rebuilding the capital stock is high. As saving flows into capital spending, the scarcity diminishes, and the real interest rate falls back to normal levels.

Next, to follow Nick's thought experiment in a slightly different way, suppose that a central bank tries to keep the real interest rate low in the face of the shock just described above. In fact, suppose that the central can manage to fix the real rental rate (hence the real interest rate) at its initial steady-state level forever.

If r(t) = r* forever, then by [1] the capital-labor ratio must remain fixed for all t > 1.

An implication of this policy is that the real wage will not fall. It's not that it cannot fall (it would fall if the real interest rate was permitted to rise). The real wage needs to fall, temporarily, to maintain full employment. But because it will not fall, then something else has to give. The level of employment must fall. Since k* = K/N is fixed and since K falls by 10%, it follows that N must fall by 10% as well. The central bank's refusal to permit the real interest rate to rise has led to an increase in unemployment (instead of a decrease in the real wage).

But things are even worse than they seem. While a shock that evaporates a part of the capital stock is eventually replenished when factor prices are market-determined, the same is not true when either the real interest rate or the real wage is fixed. In a post I wrote earlier (here), I considered a fixed real wage. But Nick's column made me realize that the same result holds if we fix the interest rate instead. A "low interest rate policy" in this case leads to "secular stagnation" (the level of output and employment is lower than it should be) as depicted in the following diagram:

One way to read this result is that it vindicates Bill Gross' idea that artificially low interest rate policy constitutes a form of "financial repression" inhibiting the U.S. recovery (I criticize his views here.)

How seriously to take this result? I'm not so sure. A lot depends on the nature of the shock that is imagined to have afflicted the economy. In the experiment considered above, I just wiped out a fraction of the economy's capital stock--like a hurricane, or nuclear bomb. A more generous interpretation is that the shock stands in for an event that evaporates a fraction of the value of existing capital (not necessarily its physical quantity). People do not become any more pessimistic in the model as a result of the shock, which is why the economy transitions back to its initial steady-state when the price-system is left unencumbered. A depressed economic outlook, on the other hand, would serve to reduce real interest rates, not increase them as in the experiment above--and that sort of scenario would provide more justification for low-interest policy.

Merry Christmas, everyone.

Consider the Solow growth model. Output (the real GDP) is produced with capital (K) and labor (N) according to a neoclassical aggregate production function Y = F(K,N).

Define y = Y/N (output per worker) and k = K/N (capital-labor ratio). Define f(k) = F(K/N,1). Then y = f(k). That is, output per worker is an increasing function of capital per worker.

If capital and labor are exchanged on competitive markets, then factor prices are equated to their respective marginal products. Let (w,r) denote the real wage and the real rental rate, respectively. Let 0 < a < 1 denote capital's share of income. Then,

[1] w = (1 - a)f(k) and r = af(k)/k

That is, the real wage is an increasing function of the capital-labor ratio (since labor becomes relatively scarce). The real rental rate for capital services is a decreasing function of the capital-labor ratio (since capital becomes relatively abundant).

Now, consider an economy populated by two-period-lived overlapping generations. People enter the economy as youngsters, they become old, and then they exit the economy. The population of young people remains fixed at N over time t = 0,1,2,... The young are each endowed with one unit of labor, which they supply inelastically at the going wage. Hence, N represents labor supply. The young save all their income and consume only when they are old. Saving is used to finance investment, which adds to the future stock of productive capital. For simplicity, assume that capital depreciates fully after it is used in production. (None of the results below are sensitive to these simplifying assumptions).

Since a young person saves his entire wage, the capital stock (per worker) evolves over time as follows:

[2] k(t+1) = (1 - a)f(k(t)) for t = 0,1,2,... with k(0) > 0 given (as an initial condition).

The transition dynamics are such that k(t) converges monotonically to a steady-state satisfying k* = (1 - a)f(k*).

The real interest rate at date t in this model is equal to the future (t+1) marginal product of capital (which is proportional to the average product of capital), R(t) = af(k(t+1)) = af((1 -a)y(t) ) / ((1-a)y(t) ).

The IS curve in this model is defined as the locus of real interest rates and output consistent with goods-market-clearing. In the present context:

[3] R(t) = af( (1-a)y(t) )/( (1-a)y(t) ).

Equation [3] describes a conventional downward-sloping IS curve. A higher level of income (because of more abundant capital) increases desired saving, which puts downward pressure on the real interest rate. Conversely, an increase in the real interest rate reduces aggregate demand.

Now, let's consider one of Nick's experiments. Begin in a steady state. Nick considers an exogenous 10% increase in the capital stock. I'll do the opposite experiment and consider a 10% decline.

The capital-labor ratio is now lower. From [1], the effect is to lower the real wage and increase the rental rate. From its depressed level, the real wage increases monotonically back to its steady-state level. From its elevated level, the rental rate declines back to its steady-state level. The real interest rate, in turn, jumps up and then declines back to its steady-state level.

In a competitive economy, these price adjustments reflect the underlying fundamentals. The shock renders capital scarce. Less capital depresses the demand for labor, which is reflected in a lower real wage. Capital scarcity means the the return to rebuilding the capital stock is high. As saving flows into capital spending, the scarcity diminishes, and the real interest rate falls back to normal levels.

Next, to follow Nick's thought experiment in a slightly different way, suppose that a central bank tries to keep the real interest rate low in the face of the shock just described above. In fact, suppose that the central can manage to fix the real rental rate (hence the real interest rate) at its initial steady-state level forever.

If r(t) = r* forever, then by [1] the capital-labor ratio must remain fixed for all t > 1.

An implication of this policy is that the real wage will not fall. It's not that it cannot fall (it would fall if the real interest rate was permitted to rise). The real wage needs to fall, temporarily, to maintain full employment. But because it will not fall, then something else has to give. The level of employment must fall. Since k* = K/N is fixed and since K falls by 10%, it follows that N must fall by 10% as well. The central bank's refusal to permit the real interest rate to rise has led to an increase in unemployment (instead of a decrease in the real wage).

But things are even worse than they seem. While a shock that evaporates a part of the capital stock is eventually replenished when factor prices are market-determined, the same is not true when either the real interest rate or the real wage is fixed. In a post I wrote earlier (here), I considered a fixed real wage. But Nick's column made me realize that the same result holds if we fix the interest rate instead. A "low interest rate policy" in this case leads to "secular stagnation" (the level of output and employment is lower than it should be) as depicted in the following diagram:

How seriously to take this result? I'm not so sure. A lot depends on the nature of the shock that is imagined to have afflicted the economy. In the experiment considered above, I just wiped out a fraction of the economy's capital stock--like a hurricane, or nuclear bomb. A more generous interpretation is that the shock stands in for an event that evaporates a fraction of the value of existing capital (not necessarily its physical quantity). People do not become any more pessimistic in the model as a result of the shock, which is why the economy transitions back to its initial steady-state when the price-system is left unencumbered. A depressed economic outlook, on the other hand, would serve to reduce real interest rates, not increase them as in the experiment above--and that sort of scenario would provide more justification for low-interest policy.

Merry Christmas, everyone.

Merry Christmas David!

ReplyDeleteGotta make Christmas pudding. Back later.

Initial thoughts:

ReplyDeleteThis is a lovely neat simple little model.

I'm with you up to this point: "Next, to follow Nick's thought experiment in a slightly different way, suppose that a central bank tries to keep the real interest rate low in the face of the shock just described above."

And I'm thinking that your thought-experiment (where a fire destroys 10% of the capital stock but the central bank does something to prevent the real interest rate from rising) should give similar answers to my thought-experiment (where there is no fire but the central bank does something to reduce the real interest rate and keep it low).

Then I keep reading and see: "But Nick's column made me realize that the same result holds if we fix the interest rate instead."

Aha! I *think* we are saying the same thing!

Now, the next question is: what is that *something* that the central bank does that causes the interest rate to fall, and causes unemployment? And my answer is: it tightens monetary policy to cause a recession.

But where we might part company (and where I would part company with Bill Gross, AFAIK) is that I see low interest rates as a *consequence* of "tight" money, and that simply telling the Fed to raise the rate of interest would actually cause the rate of interest to fall.

It's that instability question again. Like balancing a broomstick upright on the palm of your hand. If you want to move your hand North, you must first move it South, then move your hand North as the broomstick leans North.

(But this metaphor ultimately fails, like all mechanical metaphors, because broomsticks don't have expectations.)

The way for the Fed to raise interest rates, in a stable equilibrium way, would be to announce a raise in (eg) the NGDP level target. If credible, the Fed would then be forced to raise interest rates to prevent overshooting the target.

Your model has 100% depreciation, and I was assuming small depreciation in the back of my mind, but that shouldn't really matter, I think, though I'm not yet sure.

Still trying to get my head around this, but we might be converging.

PLUS 16 and sunny here in Ottawa! Last New Years Eve we were skating (illegally) on Meech Lake.

David,

ReplyDeleteThanks for this post.

But there is something I don't understand in your argument, and probably it has to do with my misunderstanding of what you mean by interest rate policy.

You assume that the central bank tries to keep the real interest rate low in the face of the capital shock, and manages to fix for ever the real interest rate at the steady-state level of the real rental rate. Then, the capital-labor ratio remains fixed for all t > 1 and, by implication, the real wage does not fall: it would fall only if the real interest rate was permitted to rise. It the real wage does not fall, unemployment follows as a result.

You thus conclude that the central bank's refusal to permit the real interest rate to rise (in other words, its low interest rate policy) leads to an increase in unemployment, instead of a decrease in the real wage.

But are you actually saying that the central bank intervenes directly on the real rental rate of capital, and seeks to hold it at a certain level? How realistic is this assumption, and how reflective is it of what is usually meant by a central bank's interest rate policy?

In a more conventional model, I would say that if the central banks aims to keep interest rates low, a capital shock of the kind you assume would actually increase the real rental rate above r*, and the adjustment should proceed as expected: savings flow into capital spending, capital scarcity diminishes, and the real rental rate falls back to its normal level r* and equals the interest rate on all other assets (net of the risk premium).

In fact, the low interest rate policy of the central bank would facilitate the adjustment, to the extent that it can set the interest rate as low as it is necessary.

Your argument would be valid if one assumes that the central bank intervenes in the capital market, buying (or selling) stocks and affecting the price of capital directly.

Under this assumption, the capital shock of your example would be resolved by the central being a "purchaser of last resort" and keeping the real rental rate of capital low by buying capital (thereby acting more as a fiscal agency than a true central bank...).

Thanks again and Merry Christmas!

Bagio,

DeleteI think that your observation (criticism) is correct.

I tried to think the experiment through assuming the existence of a government debt instrument, where the government fixed the real return on its debt, and where debt competes with capital in wealth portfolios.

The capital shock should increase the future MPK, inducing a portfolio substitution away from bonds into capital (assuming a fixed real return on bonds). And lowering the return on bonds should, if anything, speed up the capital adjustment process.

I am led to conclude, therefore, that low interest rate policy does not lead to secular stagnation (a level shortfall in employment and GDP). However, the original hypothesis remains true (that a rigid real wage can lead to secular stagnation).

Grazie, e buon natale!

My brain is still a bit slow (it is Christmas) but the easiest way to show we are thinking along the same lines is to go back to your previous model, where W/P is too high.

ReplyDeleteAssume sticky nominal W, then the Fed reduces M, which causes P to fall, and W/P to rise, same as in your model. So N falls, which causes r to fall. Exact same results, right?

Back to stuffing turkey.

Or, I think we could get the same results with sticky P and flexible W, if we make a small change to your model, so the labour supply curve slopes up (instead of being vertical). The Fed reduces M, which reduces Y, and firms (owned by old) cut N and keep existing kapital fully employed (because existing kapital has zero opportunity cost, unlike labour). Firms make super-normal profits, which are not the same as the return to kapital, which falls. And the young have lower wage income, so saving and investment fall.

ReplyDeleteA thought experiment: suppose some government entity, call it "the Fed", put a binding quota on output. Some real income would now go to quota holders, and not to wages or rents on capital, which would both fall.

ReplyDeleteThe quota is money. If P is sticky, and MV is too low, it's just like a quota on Y.

Wrote it up as a post: http://worthwhile.typepad.com/worthwhile_canadian_initi/2015/12/tight-money-as-binding-output-quota.html

ReplyDeleteNick, I'm having some trouble wrapping my head around the idea of "money as a quota," but I'll have another go at your post and reflect on it. At this point, I'm rather persuaded by the point made by Biagio above.

Deletehouldn't your real interest rate equation be

ReplyDeleteR(t)=af(k(t+1))/k(t+1)

or am I missing something? Or are you defining R(t)=r(t)k(t+1)?

Also, the difference between the rental rate and the interest rate is only that one is the present MPK and the other is the future MPK, right?

I once mused about a Solow model with a binding minimum wage in it. I think this is the same thing, just the variables are relabeled (it wouldn't be if capital depreciation wasn't 100%).

Corrected. Thanks for pointing out the error! DA

Delete"An implication of this policy is that the real wage will not fall. It's not that it cannot fall (it would fall if the real interest rate was permitted to rise)."

ReplyDeleteBut this is an assumption not an implication.

In your presentation, for the capital market to adjust to the artificially low interest rate/rental rate, MPK falls and the only way that can happen is if labor goes down, hence unemployment. Capital market clears, labor market is in disequilibrium.

But why can't we have the disequilibrium in the capital rental market? The wage adjust to a lower level, MPK stays high and simply firms wish to rent more capital then there exists. In this version, the labor market clears but the capital market is is in disequilibrium. And in this case the IS curve will be vertical.

This comment has been removed by the author.

ReplyDeleteO/T: David, what is your opinion of intertemporal budget constraints? David Glasner has a new post on them here.

ReplyDelete